This article is also available as PDF.

Introduction

As instances of default under collateralized debt obligations (CDOs) rise, uncertainty over the resolution of eventual disputes takes on increasing significance for parties to derivatives investments. Nowhere is this better demonstrated than in the enforcement of rights under credit default swaps. By 2008, outstanding credit default swap contracts had a combined market value of more than US$2 trillion((Per Moody’s Investors Service, May 2008)).

Synthetic vs Cash CDOs

CDOs are a form of asset-backed security under which a special-purpose vehicle (SPV) is established to hold cash-producing assets carrying various levels of risk and reward. The SPV issues bonds or other securities to investors in tranches which reflect the productivity of the assets from which their value is ultimately derived. Often the SPV is an offshore corporation established to avoid or minimize tax otherwise payable to the revenue authorities of the U.S., Canada and other industrialized countries.

Securities issued through CDOs are derivative in nature, funded through either a portfolio of cash assets such as bonds or mortgage-backed securities (“cash CDOs”), or a portfolio of credit default swaps (“synthetic CDOs”). Parties to synthetic CDOs enter into contractual arrangements which expose the SPV to credit risk in exchange for periodic payments. The

arrangement is roughly equivalent to an insurance contract in which the SPV insures its counterparty against defaults on its own mortgage portfolio or against specified losses which it may incur from other financial obligors in the course of its business (the “reference portfolio”).

Uncertainties Arising from Leverage

By their nature, synthetic CDOs carry with them a number of inherent uncertainties rendering them more susceptible than cash CDOs to litigation. To maximize leverage, CDOs are structured so as to minimize cash reserves. Collateral is posted equating to an agreed portion of the aggregate potential exposure of the credit protection purchaser. Agreements between swap counterparties specify circumstances (called “material adverse events”) under which collateral must be augmented. Whether such events have taken place will depend on the terms negotiated and then current financial circumstances.

In exercising its remedies the secured party must balance its interests against its contractual obligations. If it purports to terminate or demands excessive collateral, its good faith may be called into question. Good faith is a term often implied by the courts and specified under standard contractual terms such as those of the International Swaps and Derivatives Association (ISDA)((The ISDA represents participants in the privately negotiated derivatives industry. Since its inception, the ISDA has pioneered efforts to identify and reduce the sources of risk in the derivatives and risk management business)).

Similarly, there may be a question whether a material adverse event has occurred, and/or have triggered termination rights under the ISDA’s 1992 and 2002 Master Agreements or other comparable documents, if the party or its credit support provider merges or amalgamates with another party under circumstances where the creditworthiness of the merged vs premerger body is arguable. Valuations may be necessary to determine the relative values.

Valuations of assets within the reference portfolio may also be necessary and these may give rise to difficulties. In High Risk Opportunities HUB Fund Ltd. v. Credit Lyonnais((High Risk Opportunities HUB Fund Ltd. v. Credit Lyonnais, N.Y. Sup. Ct. July 07, 2005))a derivatives case involving non-deliverable forwards linked to currency fluctuations, the financial institution was found to have improperly valued the subject contracts upon the occurrence of an event of default. The counterparty successfully argued that Credit Lyonnais’ market quotations were not obtained in good faith and that it interfered with market-makers’ independence in the valuation process. Credit Lyonnais, by urging an improper interpretation, not only reduced High Risk’s termination balance but limited its own margin call obligations, subjecting itself not only to a large difference but to claims that High Risk’s insolvency had been caused by the valuation.

The consequences of making the wrong decision are made more severe by short time fuses for increasing collateral, potentially leading to interlocutory injunction hearings. Several U.S. financial institutions have been sued on notices to substantially increase collateral, for example and CDO Plus Master Fund Ltd. v. Wachovia Bank, N.A.((CDO Plus Master Fund Ltd. v. Wachovia Bank, N.A., 07-11078, S.D.N.Y. Dec. 7, 2007)). In Canada, parties seeking injunctive relief may be required to post an undertaking in damages and security in support thereof, which may have similar effect to the collateral required under the agreement.

The effect of leverage is evident in UBS v. Paramax Capital Int’l((UBS v. Paramax Capital Int’l, Civ. No. 07604233, Sup. Ct. N.Y. Co., commenced Dec. 26, 2007)), in which a hedge fund agreed to provide protection on over US$1.3 billion in CDOs and was only required to post some $4.5 million in collateral. Unfortunately, the CDOs were backed by subprime mortgage investments, and as the portfolio assets were written down, UBS made collateral calls increasing the total required collateral by approximately 1,400%. This gave rise to arguments in litigation that UBS had entered into the transactions without disclosing the true nature of the assets, misrepresenting its write-down policy and failing to disclose accounting benefits which it would derive from entering into the credit default swap.

Choice of Law and Jurisdiction of Dispute Resolution

Parties structuring synthetic CDOs should pay particular attention to jurisdictional and choice of law provisions which may come into conflict in the plethora of applicable contracts. This is exemplified in the multijurisdictional litigation of UBS AG and UBS Securities LLC et al v. HSH Nordbank AG((UBS AG and UBS Securities LLC et al v. HSH Nordbank AG, [2009] EWCA Civ 585 (Eng. CA))) (English Court of Appeal) with the parties reversed in the New York Supreme Court((HSH Nordbank AG v. UBS AG and UBS Securities LLC, N.Y. Sup. Ct. no. 08/600562)).

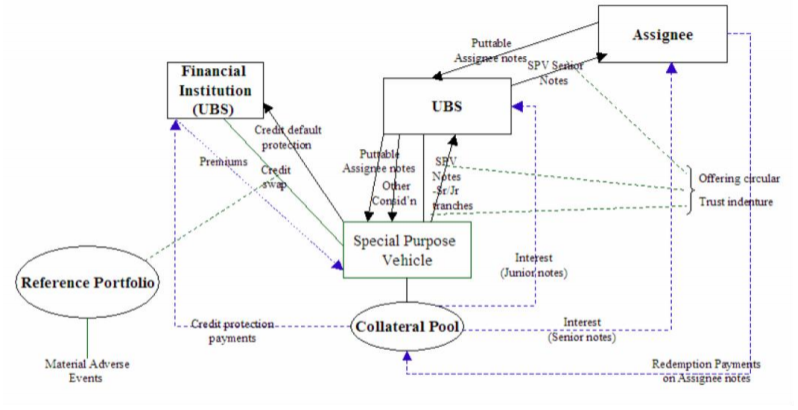

The synthetic CDO in UBS was structured roughly as follows:

The complexity of the arrangement included different choice of law and jurisdictional clauses:

- Agreement under which Assignee would issue notes to dealers (including UBS) as part of a pre-existing programme, and Information Memorandum relating to same: governed by English law; England non-exclusive jurisdiction for disputes

- UBS-Assignee letter agreement re intended structure and sale of Senior SPV Notes to Assignee: governed by New York law; no jurisdiction clause

- Pricing Supplement and Dealer’s Confirmation re issuance of the Assignee notes: governed by English law; England exclusive jurisdiction for disputes

- Offering Circular and Trust Indenture re linkage between SPV notes and Reference Pool assets, and triggers for credit protection payments and corresponding reductions in balance due under SPV notes: governed by New York law; New York non-exclusive jurisdiction for disputes

- Credit Swap governing credit premium payments and credit protection payments in event of credit events. The Credit Swap incorporated by reference ISDA Master Agreement: governed by English law; England nonexclusive jurisdiction for disputes

- Reference Pool Side Agreement governing UBS’ management of the reference portfolio and monitoring its credit quality: governed by New York law; New York non-exclusive jurisdiction for disputes.

On February 25, 2008, proceedings were commenced in New York by the Assignee’s successor. Allegations included breach of contract in the sale of SPV notes to the Assignee; fraudulent or egligent representations inducing the Assignee to have purchased the SPV notes; breach of fiduciary duty and breach of a duty of good faith relating to UBS’ management of the Reference Portfolio; unjust enrichment and conversion.

On the same day, UBS filed suit in London seeking a declaration that the essence of the dispute falls within the jurisdiction of the English courts by virtue of the Dealer’s Confirmation. The presiding judge disagreed and the matter was unsuccessfully appealed to the Court of Appeal for England which, noting contradictory jurisdictional provisions, had to analyze the various agreements and the substance of the dispute before it((Supra, note 6, per Lord Collins of Mapesbury at paras. 83-84)):

But the essential task is to construe the jurisdiction agreement in the light of the transaction as a whole. As I suggested in Satyam Computer Services Ltd v Upaid Systems Ltd [2008] EWCA Civ 487, [2008] 2 All ER (Comm) 465, at [93], whether a dispute falls within one or more related agreements depends on the intention of the parties as revealed by the agreements.

Plainly the parties did not actually contemplate at the time of the conclusion of the contracts that there would be litigation in two countries involving allegations of misrepresentation in the inception and performance of the agreements. But in my judgment sensible business people would not have intended that a dispute of this kind would have been within the scope of two inconsistent jurisdiction agreements. The agreements were all connected and part of one package, and it seems to me plain that the result for which UBS contends would be a wholly uncommercial result and one that sensible business people cannot have intended.

Given the plethora of agreements and potential issues arising in respect of synthetic CDOs, parties entering into them should pay particular attention to avoid jurisdictional and choice-of-law clashes which may contribute to the already costly and time-consuming nature of litigation in these matters.

Conflicts of Interest

As demonstrated in UBS, synthetic CDO arrangements may involve an inherent conflict of interest in which a party’s duties are difficult to discharge. In UBS, the financial institution that monitored the reference portfolio potentially stood to gain from allowing lower quality assets to enter the pool, since material adverse events would trigger credit protection payments to the detriment of the Assignee. Although the parties specifically contemplated this potential conflict in entering into the “Reference Pool Side Agreement”, it is nevertheless difficult for a conflicted party to discharge its obligations of good faith under such contracts.

For example, in High Risk v. Credit Lyonnais, supra, the financial institution was found to have interfered with marketmakers’ independence in valuing the subject contracts, having a fundamental impact on resolution of the claim and, it was argued, on the very solvency of the counterparty.

Other Securities Law Claims

Synthetic CDOs are also particularly vulnerable to arguments advanced to impugn securities transactions generally. Here are but a few examples:

- Claims against investment advisors based on suitability and know-your-client rules. In 2007, Aastra Technologies Limited commenced legal proceedings against its investment advisor, HSBC Securities (Canada) Inc. and one of its employees, in the Ontario Superior Court of Justice seeking damages relating to investment advice provided with respect to Aastra’s purchase of $13.7 million of investments in non-bank asset-backed commercial paper (ABCP) that were frozen following the U.S. subprime mortgage industry collapse. The claim alleged that the employee had described ABCP as primarily baskets of residential mortgages with limited car loans and credit card debt, bundled to produce a “high-quality, short-term investment product”.((link expired)) A large number of similar claims have arisen in the United States since the subprime meltdown.

- In addition to derivatives investments being relatively risky, they can be subject to specific statutory, regulatory or contractual prohibitions knowledge of which may be imputed to the investment advisor. In Daniel Boone School Dist. v. Lehman Bros. Inc.((Daniel Boone School Dist. v. Lehman Bros. Inc., 187 F. Supp. 2d 400 (W. D. Pa. 2002)))10 for example, not only did the advisor face liability in the face of a prohibitory state statute but the issuer faced liability as a co-conspirator.

- Claims of misrepresentation in marketing materials and pre-contractual negotiations. Well-drafted offering memoranda, trust indentures and other CDO agreements will include disclaimers effective in most circumstances. See for instance, Banco Espirito Santo de Investimento, S.A. v. Citibank, N.A.((Banco Espirito Santo de Investimento, S.A. v. Citibank, N.A., 2003, S.D.N.Y. 2d Cir.))

In conclusion, while synthetic CDOs and credit default swaps carry with them leverage and hedging opportunities, parties considering such transactions should give due attention to legal uncertainties which may arise from their complexity.

Related blog posts: Securities Law for the Small Business, or When Does Securities Law Apply to Me? | The Curative Provision in Section 43(6) of the Personal Property Security Act: How Misleading is a Seriously Misleading Error?